– January Market Snapshot –

– January Market Snapshot –

- Equity markets consolidated the large gains made in late 2023, with valuations advancing further in January.

- Bond yields reversed a small portion of the large decline recorded over November and December.

- The $A depreciated last month, following 2 months of appreciation.

International Equities

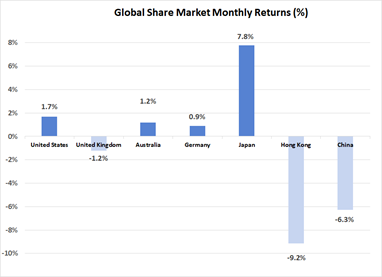

There were mixed results across major global equity markets over January. The United States (up 1.7%) once again benefited from a strong performance by the large technology sector, with earnings results helping justify the recent share price growth. Support for the Japanese market was buoyed by a weaker Yen (which makes exporters more competitive), as well as further evidence that Japanese companies were taking action to improve return on equity, primarily via share buy backs. The Nikkei Index jumped 7.8% as a result, bringing the quarterly gain to 16.9%. European markets were weaker, with a flat result for the month, reflecting general sentiment that both economic and company earnings growth would be modest in the year ahead.

Emerging markets followed a similar pattern to that of recent months, with large falls on the Chinese market dragging the category lower. A 9.2% decline in Chinese equities came despite news that the Chinese central bank (the People’s Bank of China) had lowered bank reserve requirements in an attempt to encourage greater lending. Data was also released showing the Chinese economy continues to expand, at the relatively healthy rate of 5.2% per annum. Other emerging markets were mixed, with India (up 2.2%) continuing its strong run, whereas the South Korean market declined 6.7%.

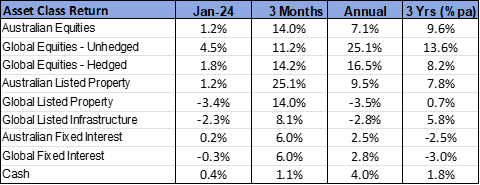

A small increase in global bond yields triggered a slight reversal of the rally in global listed property last month, with the sector declining 3.4%. There was a similar pattern displayed by the global listed infrastructure asset class, which dropped 2.3% in value. In addition to higher bond yields reducing the relative attractiveness of yields from these assets, the lower level of inflation now in place is likely to reduce the scope for earnings growth. The Australian listed property sector moved against this trend, with a gain of 1.2%, bringing the quarterly increase to 25.1%. Industrial property specialist, Goodman Group, accounting for 31% of the asset class, has made a major contribution to this gain. Goodman has returned 24.2% over the past quarter.

Australian Equities

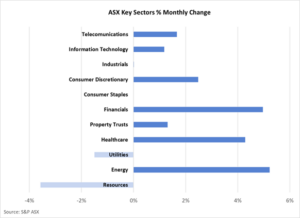

The Australian share market marginally underperformed the global average, with the S&P ASX 200 Index rising 1.2% last month, bringing the Index to a new all-time high. A 5.9% rise in the global oil price boosted the energy sector, which was the strongest performer with a gain of 5.2%. It was also a solid month for the finance sector, with both banks and insurance companies contributing to the 5.0% increase.

Reversing the pattern from the previous month, resources were the weakest sector over January. Following a period of strong price gain, a 6.7% decline in the iron ore price saw losses from major mining companies, with BHP falling 6.2%. Mining stocks with lithium exposure were also weaker, with Mineral Resources (down 14.4%) and Pilbara Minerals (down 10.1%), extending their decline recorded over 2023.

The profit reporting season for the period ending December 2023 takes place over February and may have a significant impact on individual stock price movements in the month ahead.

Fixed Interest & Currencies

Following the sharp decline in bond yields in the final two months of 2023, yields were relatively stable over January. Both Australian and U.S. 10-year government bond yields rose 0.1% to finish the month at 4.0%. There was no movement in cash interest rates across major economies, with the RBA maintaining the 4.35% cash target following its meeting in early February. The release of the December quarter Consumer Price Index data confirmed that Australia’s inflation rate was continuing to decline, adding to the market’s confidence that cash interest rates will fall over the course of 2024. Annual inflation at the end of December was 4.1%, down from 5.4% three months earlier.

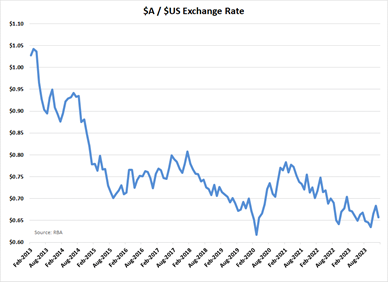

Following two months of appreciation, the $A declined from U.S. 68.4 cents to U.S. 65.7 cents. The weaker iron ore price, as well as some strengthening in the $US, contributed to the lower $A. The Australian currency was also 1.7% weaker against the Euro, but appreciated 0.3% against the Japanese Yen. As indicated on the accompanying chart, the $A has been on a longer term downward trend since peaking at around U.S. 78 cents in February 2021.

Outlook and Portfolio Positioning

The current mood on financial markets contrasts significantly with that prevailing 18 months ago, when a rapid rise in interest rates triggered a very strong consensus view that the global economy was heading for recession. Subsequent events have highlighted just how wrong market consensus can be. Now that the mood has turned unequivocally bullish, with the “soft-landing” scenario of normalised inflation and ongoing economic expansion firmly baked into expectations, the danger for the year ahead is that market consensus is once again proved incorrect.

Commentary from both the U.S. Federal Reserve and the Australian Reserve Bank, following recent Board meetings, appeared to be designed to soften some of the market’s optimism around inflation that forms the core of the current consensus view. In its statement following the February Board Meeting, the RBA made the following warning that there was still a possibility that inflationary pressure could lead to another increase in interest rates:

“While recent data indicate that inflation is easing, it remains high. The Board expects that it will be some time yet before inflation is sustainably in the target range. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks, and a further increase in interest rates cannot be ruled out.”

Should there be an upside surprise to inflation, then significant negative effects on both equity and bond markets may be the result. A spike in oil prices, or ongoing increase in wages, could be two factors that disrupt the current downward trajectory in price growth.

Hence, whilst the optimistic mood on financial markets is warranted, investors should not assume that the orderly path to target inflation that has been assumed will be delivered without incident. A cautious approach to asset allocation remains prudent. The dangers in chasing returns in the more interest rate sensitive sectors that have rallied strongly in recent months, such as Australian listed property and long dated bonds, should be understood. Assets less dependent on the falling inflation assumption, such as emerging market equities, may present more valuable diversification benefits than is normally the case. History has demonstrated that when market participants are near peak exuberance, underlying investment risks may be at their highest.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665