- The rally on global share markets continued as confidence in the economic outlook continued to improve.

- Inflation data continues to soften.

- U.S. bond yields rose despite the lower inflation pressure.

International Equities

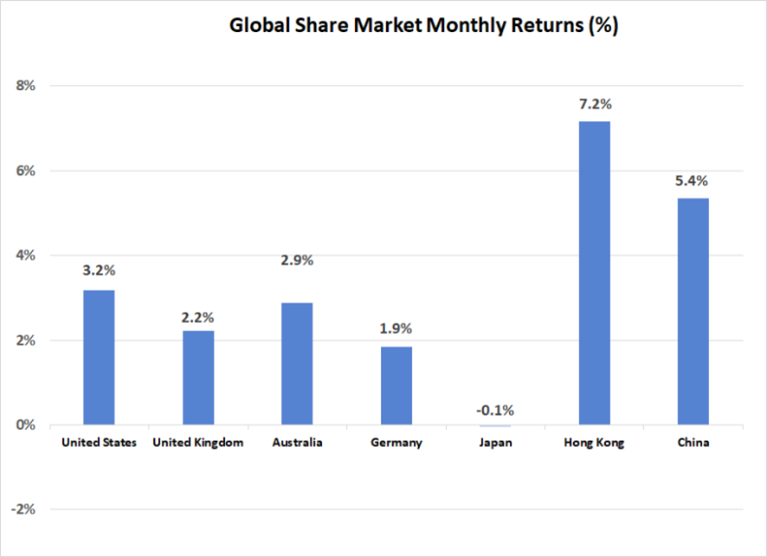

The commencement of the profit reporting season in the United States provided share markets with more confidence, with prices continuing move higher in July following a very strong June. Although there were some earnings misses, strong results from companies such as Alphabet and Meta contributed to a 3.2% gain on the S&P 500 Index. Notably, the U.S. banking sector reported better than expected results for the period ending June 30th. European markets were also solid, despite a 0.25% rise in interest rates by the European Central Bank. Following two months of sharp increase, the Japanese market consolidated its position in July, with a flat result. A change to the Japanese central bank’s yield curve control, allowing more scope for yields to increase from current lows, may have diminished support for Japanese equities.

For the second consecutive month, the Hong Kong and Chinese equity markets outperformed the global average. Although economic growth data in China has continued to paint a dim picture, investors took confidence from statements made by leaders following the July Politburo meeting. Commitments to “actively expand domestic demand” and to “expand consumption by raising income levels” were made by Chinese leaders. These statements followed the release of June quarter national accounts figures, which indicated an economic expansion of just 0.8% over the 3 month period. A lack of inflation in China may provide some additional scope for expansionary policies in coming months.

Outside of China, it was generally also a strong month for other emerging economy share markets. The MSCI Emerging Market index gained 4.9% (in $A terms), placing it ahead of the overall global developed market average of 2.1%. A significant rise in the global oil price of 16.1% boosted support for Middle Eastern markets. Saudi Arabia’s expected lengthening of supply cuts, combined with likely lower volumes from Russia, contributed to the higher oil price last month.

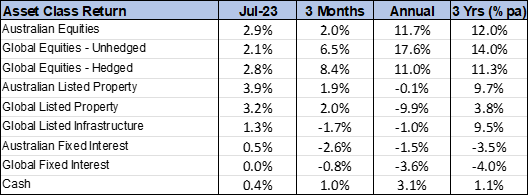

It was a solid month for real assets, with both infrastructure and property posting gains. The absence of any further fallout from the U.S. banking sector has restored some confidence in global listed property. However, despite recovering over the past 2 months, the asset class remains 9.9% below its level of 12 months ago.

Australian Equities

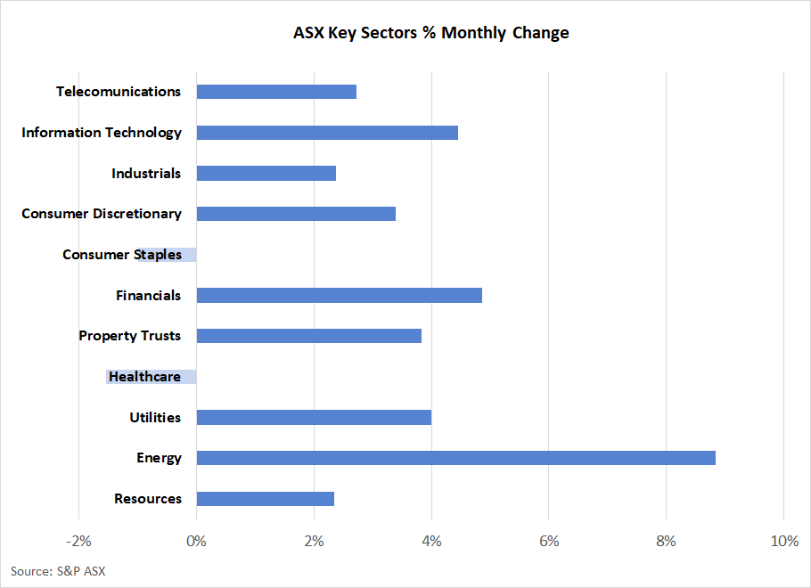

The Australian market was broadly in line with the global average over July, with the S&P ASX 200 Index rising 2.9%, to bring the annual gain to 11.7%. Given the significant rise in global oil prices, energy was the standout sector last month, rising in value by 8.8%. Financial stocks also made a solid contribution to the overall market gain. The pause in interest rate increases by the RBA may have boosted confidence in the banking sector, as further interest rate increases may have put additional downward pressure on bank interest margins.

The more defensively positioned healthcare and consumer staples sectors were the only negative performers over July. As was the case in June, healthcare’s decline can be attributed to CSL Limited (down 3.2%), with June’s earnings downgrade continuing to hamper support for the stock. Woolworths (down 2.8%) led the consumer staples sector lower. Woolworth’s decline could be valuation related, with strong price growth from a low in November last year pushing the stock to a challenging price of 28 times earnings.

The more defensively positioned healthcare and consumer staples sectors were the only negative performers over July. As was the case in June, healthcare’s decline can be attributed to CSL Limited (down 3.2%), with June’s earnings downgrade continuing to hamper support for the stock. Woolworths (down 2.8%) led the consumer staples sector lower. Woolworth’s decline could be valuation related, with strong price growth from a low in November last year pushing the stock to a challenging price of 28 times earnings

Fixed Interest & Currencies

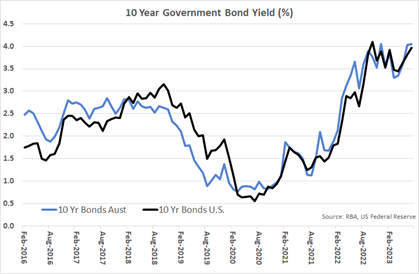

Australian cash interest rates remained unchanged at 4.1% following the RBA meetings in both July and August. A fall in the annual inflation rate from 7.0% to 6.0% between March and June provided the central bank with enough evidence that interest rates were high enough – for now at least. With the cash rate stable, there was little change in the 10-year government bond yield, which stands at 4.05%. In the United States, however, the Federal Reserve shifted cash rates higher by a further 0.25%, with the 10-year Treasury bond yield also rising from 3.81% to 3.97% over July. These higher interest rates came despite data showing that inflation in the U.S. was on a steady downward path.

The $A consolidated the gains made in June, with a further increase of U.S. 0.5 cents to U.S. 66.8 cents. However, this latest increase reflected a weaker $U.S., with the $A depreciating slightly against both the Euro and Yen last month.

Outlook and Portfolio Positioning

Recent optimism displayed on equity markets has been built on the growing assumption that company earnings can remain largely immune from a downturn in the broader economy. A necessary precondition for this assumption is that any economic downturn will be relatively mild. It is widely accepted that conditions in labour markets are the ultimate barometer of the seriousness of periods of economic weakness. A rise in unemployment is the one variable that can fundamentally damage aggregate demand and then create second and third round impacts on economic growth. With inflation now somewhat under control, it is labour markets, and more specifically unemployment, that should be a primary focus of those looking to assess the future direction of the economy, company earnings and share prices.

To date, labour markets have been remarkably resilient. In Australia, for example, demand for labour has remained particularly buoyant, driving a 3.0% growth in the number workers employed over the year to June 2023 and a 4.7% increase in hours worked. Such has been the strength of the labour market, that in May, the workforce participation rate (i.e. the percentage of the adult population employed or seeking employment) hit a record high of 66.9%. Like many economies overseas, Australia is enjoying what is effectively deemed to be full employment with the unemployment rate at 3.5%.

Unfortunately, however, the strength of the labour market is not being matched by growth in output, resulting in a significant decline in labour productivity. In fact, the 4.5% fall in output per hour worked in Australia in the year to March 2023 was the largest decline in productivity for more than 40 years. With wage costs on the rise and consumer spending starting to show signs of softening, the sustainability of current strong conditions in labour markets must come under question. Potentially firms have responded to the past 2 years of labour shortages by “hoarding workers”, which has delayed the transmission between weaker output growth and softer demand for workers. In addition to the impact of the softening in the economic cycle, labour markets will also have to absorb the effects of a scaling back of several State Government led infrastructure projects.

Recent exuberance on share markets may therefore be somewhat premature. Certainly the signs that inflation may be pulling back materially from earlier peaks are promising. However, the conclusion that inflation can be brought under control without significant deterioration in labour markets and company earnings may prove to be misplaced. Aggressively chasing the latest equity market rally should therefore be avoided. Of more certainty, though, is that interest rates above 4% in a period of normalising inflation offer more value than they have for some time.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR (composite of 50% hedged and 50% unhedged), FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HK, MSCI United Kingdom TR, Nikkei 225 in JP, S&P 500 TR in US.

General Advice Disclaimer (to be replaced by Practice Specific Disclaimer)

This document has been prepared by Plain English Economics Pty Ltd, trading as “Brad Matthews Investment Strategies” (BMIS). Plain English Economics Pty Ltd is a Corporate Authorised Representative of First Point Wealth Management P/L (AFSL 483004). The document is intended for the use of financial adviser clients of BMIS and their staff only. Any advice provided is of a general nature and does not take into account personal circumstances. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance.