September 2025: Positive sentiment pushes global shares higher

- The rally on global share markets continued over September, with the US and emerging markets particularly strong.

- Falling US bond yields added to the positive equity market momentum.

- The Australian share market lagged, with a pull-back from the August highs.

International Equities

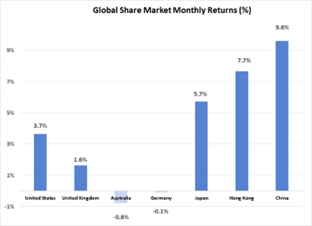

An easing in monetary policy by the United States Federal Reserve Bank appeared to lift investor sentiment across both bond and equity markets last month. The U.S. share market once again outperformed, with the S&P 500 Index gaining 3.7%. Information technology stocks came back into favour after a brief lull in support during August. Nvidia’s 7.1% increase made a major contribution to the overall market gain, with the chip manufacturer now more than 50% ahead over the past year. Tesla’s share price continued to take a volatile path, increasing by 33.2% over September, ahead of releasing impressive production numbers for the third quarter. The support for smaller companies in the U.S. also continued last month, with the Russell 2000 Index gaining a further 3.1% to be 12.4% ahead for the quarter.

Outside of the U.S., share market performance was mixed. Across Europe, sentiment was softer, with the German market declining 0.1% and the French market gaining 2.5%. The U.K. market (up 1.6%) performed relatively well, despite a 2.6% drop in the crude oil price. As was the case in August, Asian markets showed significant growth. Japan’s Nikkei Index gained 5.7% and is now 11.6% higher for the quarter. The ongoing refocus on shareholder returns across corporate Japan has continued to attract buyers to the Japanese equity market.

China’s share market rally also continued, with a 9.6% jump in September bringing the quarterly gain to 19.8%. China’s rally has defied the broader state of the local economy, which continues to appear subdued. Strong investor interest in the technology sector and artificial intelligence applications has been one contributor to the recent resurgence in Chinses equities. The majority of other emerging economy share markets were positive over September, with India’s 1.2% gain reversing a small component of the recent losses recorded there.

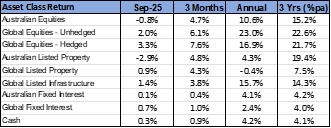

With the reduction in interest rates in the United States, solid support for real assets was maintained, with global listed property returning 0.9% and listed infrastructure rising by 1.4%. The Australian listed property sector was an exception, though, with A-REITs declining by 2.9% following a period of strong growth. Goodman Group led the sector lower, with a 4.6% fall in price. Despite the broader support for data centres globally, Goodman has now declined 10.6% over the past year, as investors have become concerned over the lofty valuations the stock had reached.

Australian Equities

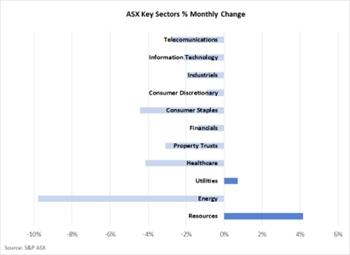

The Australian share market was one of the weakest performing across developed markets last month, with the S&P ASX 200 Index falling by 0.8%. In annual terms, Australian equities have increased by 10.6%, which is now well short of the global average increase of 16.9%.

Energy (down 9.8%) was the sector making the largest contribution to the Australian market decline. A slightly weaker oil price, as well as the withdrawal of a takeover offer for Santos (down 13.9%), created a difficult month for the energy sector. Investors also continued to shy away from selected stocks that performed poorly in the August profit reporting season, with Woolworths and CSL both down 5.8% and extending the losses recorded in August. The rotation away from the Commonwealth Bank also continued, with the CBA’s 2.0% decline in September bringing its quarterly fall to 8.3%.

Resource stocks (up 4.1%) were the best supported across the Australian market last month. Iron ore prices continued to strengthen and have now appreciated 11.5% over the past quarter. BHP (up 0.6%), however, only experienced minimal participation in the resource rally, as a result of concerns stemming from a state‑owned iron ore importer in China instructing their steel mills to temporarily halt purchases from BHP due to a pricing dispute. The ongoing rally in the gold price was another source of support for Australian resource stocks. Gold’s price rise was also a notable contributor to the ongoing rally in smaller companies, with the Small Ordinaries Index rising 3.4% over the month.

Fixed Interest & Currencies

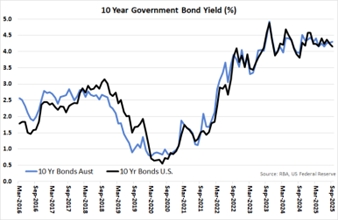

The main focus of bond and money markets over September was the U.S. Federal Reserve Bank’s decision to reduce cash interest rates by 0.25% to the target range of 4.0% to 4.25%. Confirmation of the lower cash interest rate also led to a decline in longer term yields, with U.S. 10-year Treasury Bond yields dropping from 4.23% to 4.16%.

The main focus of bond and money markets over September was the U.S. Federal Reserve Bank’s decision to reduce cash interest rates by 0.25% to the target range of 4.0% to 4.25%. Confirmation of the lower cash interest rate also led to a decline in longer term yields, with U.S. 10-year Treasury Bond yields dropping from 4.23% to 4.16%.

This decline, however, was not matched in Australia, where stronger consumer spending and higher than expected monthly inflation results have reduced the probability of a further easing in interest rates this year. As a result, the Australian 10-year Government Bond yield increased slightly from 4.28% to 4.31%.

With interest rates declining in the U.S., the downward momentum in the $US continued, enabling the $A to appreciate from US 65.4 cents to US 66.0 cents. The $A was also stronger against the Yen by 1.9% and also 0.8% higher relative to the Euro.

Outlook and Portfolio Positioning

The September interest rate reduction in the United States has provided equity markets with another reason to rally. As appears to be pattern of late, good news is quickly reflected in share market prices and bad news is ignored or put aside to be considered at a later date. Today’s share market is being driven by a combination of very positive investor sentiment, strong market liquidity and a robust corporate sector that has provided just enough evidence of earnings growth to justify current valuations. In the short-term, there appears little that may dent these 3 drivers of market performance and the rally may therefore continue for some time.

However, whilst the reaction to the Federal Reserve’s rate cut was overwhelmingly positive, a share market with less sanguine sentiment may well have reacted very differently. In essence, the Federal Reserve’s decision was driven by the evidence of a material weakening in labour market growth. Softer conditions in labour markets are generally considered to be evidence of a later stage downturn in the economic cycle, which should have negative implications for company earnings. Unlike Australia, it is more difficult to argue that success in lowering inflation was the primary motivation behind the Federal Reserve’s monetary policy easing. Core or underlying inflation in the U.S. is still approximately 1% above the central bank’s 2% target. With the impact of the tariff program still to be determined, the central bank should be very hesitant in engineering a softer policy on the basis that inflation objectives have been met.

The share market’s willingness to discount risks in the current cycle was again demonstrated in September by the lack of reaction to the shutdown of government services triggered by the absence of agreement between Congress and the President to authorise government spending for the new fiscal year. Whilst relatively common, and unlikely to have any lasting impact, there is an environment of heightened policy uncertainty in the U.S. . The fact that the U.S. share market trades at an all-time record high at a time when much of the government’s expenditure has been frozen highlights the dominance of positive sentiment on today’s share market.

However, the U.S. is not the only share market characterised investor exuberance. China’s rally in recent months has come despite any long awaited domestic economic recovery or government stimulus program. Whilst the cheaper valuations that were available in the Chinese market may provide a firm basis for this rally, the recent uplift in market valuations comes at a time when there remains uncertainty over the magnitude and impact of U.S. tariffs applying to Chinese exports – and the new world trade order more broadly. It is somewhat ironic and a direct affront to economic theory (which espouses the benefits of free trade) that the world’s two largest economies, with potentially the most to lose from new trade barriers, have experienced such strong share market rallies in the months since the announcement of the U.S. tariff program.

As discussed above, there are many reasons to question both the basis for, and the sustainability of, the current share market rally. However, the generally strong position of companies, the potential for significant positive transformation to be delivered by artificial intelligence, and the very strong health of the financial sector are all factors that can’t be ignored and may continue to drive share markets higher. As such, whilst a cautious approach to equity market exposure should be maintained, the lack of any financial dysfunction in markets, or apparent near-term catalyst to dent sentiment, suggests the majority of longer-term target allocations to equity markets should be maintained for now at least.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), MSCI China (Composite) in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665