July 2025: A solid start to the new financial year for equity markets

- Global share markets continued to trend higher, ignoring the potential for any negative surprises in the finalisation of the U.S. tariff program.

- Longer term bond yields increased, despite ongoing expectations of lower cash rates.

- The USD steadied over the month, following a period of weakness.

International Equities

Investor sentiment remained positive over July, with global equity markets advancing by an average of 2.1% in their third consecutive monthly gain. Further detail on the U.S. tariff program failed to concern investors, despite tariff rates being introduced for many countries above the 10% “baseline”. Examples of the higher tariffs applying include the rate of 15% on imports from Europe and Japan, 35% for Canada, 39% for Switzerland, 20% for Taiwan and Vietnam and 25% for India. Negotiations around a tariff deal with China are ongoing. Although Australia has not finalised a “deal” with the U.S., it is anticipated the 10% base-line rate will apply (although 50% product specific tariffs will be charged on steel, aluminium and copper).

Investor sentiment remained positive over July, with global equity markets advancing by an average of 2.1% in their third consecutive monthly gain. Further detail on the U.S. tariff program failed to concern investors, despite tariff rates being introduced for many countries above the 10% “baseline”. Examples of the higher tariffs applying include the rate of 15% on imports from Europe and Japan, 35% for Canada, 39% for Switzerland, 20% for Taiwan and Vietnam and 25% for India. Negotiations around a tariff deal with China are ongoing. Although Australia has not finalised a “deal” with the U.S., it is anticipated the 10% base-line rate will apply (although 50% product specific tariffs will be charged on steel, aluminium and copper).

The potential consequences from the tariffs of higher inflation and lower economic growth in the U.S. did not deter investors, with the U.S. S&P 500 Index rising 2.2% over the month. Once again it was the large technology stocks leading the U.S. market higher, with Nvidia’s 12.6% gain being particularly notable. Tesla (down 3.0%) was the only one of the “Magnificent 7” technology stocks to decline last month, with Tesla now 23.8% lower over the past 6 months.

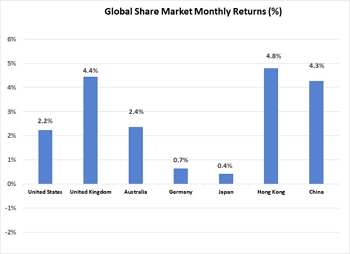

Outside of the U.S., gains were more modest in Europe and Japan, where markets advanced less than 1%. The United Kingdom was an exception, with a jump in the global oil price contributing the U.K.’s 4.4% market rally. It was also another strong month for emerging markets, with China advancing a further 4.3%. The higher oil price also buoyed Middle Eastern markets. These gains were supported by South Korea (up 6.9%) and Taiwan (up 7.7%), although India detracted from the emerging market average, with a loss of 3.1%.

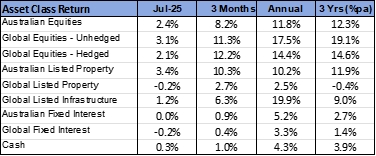

As was the case in June, listed real assets did not keep pace with the broader share market. Slightly higher bond yields may have detracted support from global listed property (down 0.2%) and infrastructure (up 1.2%). Support for Australian listed property was stronger, with the sector rallying 3.4%. Expectations of lower cash rates may be contributing to support for Dexus, GPT and Scentre Group, all of which increased in value by more than 5% last month.

Australian Equities

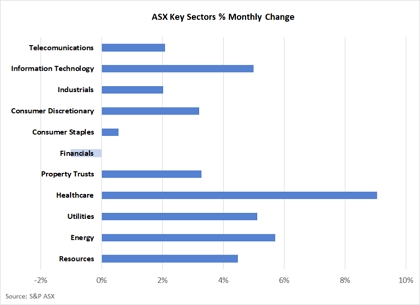

The Australian market performed slightly better than the global average in July, with the S&P ASX 200 Index rising 2.4%. In a marked turnaround in relative performance, healthcare was the strongest performer with a gain of 9.1%. CSL Limited (up 13.1%) was the main contributor to the sector’s gains. CSL’s advance appears to have come at the expense of the banking sector, with a rotation in support away from the Commonwealth Bank (down 3.7%) evident late in the month.

The Australian market performed slightly better than the global average in July, with the S&P ASX 200 Index rising 2.4%. In a marked turnaround in relative performance, healthcare was the strongest performer with a gain of 9.1%. CSL Limited (up 13.1%) was the main contributor to the sector’s gains. CSL’s advance appears to have come at the expense of the banking sector, with a rotation in support away from the Commonwealth Bank (down 3.7%) evident late in the month.

Resource and energy stocks were also well supported, with both oil prices (up 6.4%) and iron ore prices (up 4.9%) increasing investor confidence in these sectors. BHP Limited was a significant beneficiary, with the stock rallying 6.8%.

Fixed Interest & Currencies

There was little movement at the front end of yield curves, with cash rates unchanged in July across Europe, the United States and Australia.

However, a lower-than-expected June quarter inflation result in Australia, showing annual inflation has dropped to 2.1%, has increased the prospects of an August cash rate reduction by the RBA.

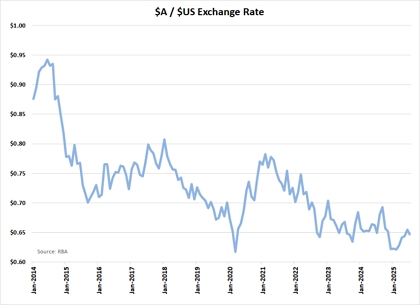

Despite the favourable inflation result, longer term Australian yields still increased over the course of July, with the 10-year Government bond yield rising from 4.16% to 4.32%. This increase was consistent with the movement in the 10-year U.S. Treasury Bond yield, which rose 0.13% to 4.37%. The small increase in bond yields over the month resulted in a fall in bond prices and broadly flat returns for the asset class. After declining for the majority of the 2025 calendar year, the $US firmed slightly last month. The absence of any indication of an immediate reduction in U.S. cash interest rates may have added support to the $US. This strength in the $US resulted in the $A declining from U.S. 65.5 cents to U.S. 64.7 cents. However, with the iron ore price increasing and some ongoing improvement in sentiment around the Chinese economic outlook, the $A was relatively well supported over the month and increased 2.1% against the Yen and was 1.3% higher relative to the Euro.

Despite the favourable inflation result, longer term Australian yields still increased over the course of July, with the 10-year Government bond yield rising from 4.16% to 4.32%. This increase was consistent with the movement in the 10-year U.S. Treasury Bond yield, which rose 0.13% to 4.37%. The small increase in bond yields over the month resulted in a fall in bond prices and broadly flat returns for the asset class. After declining for the majority of the 2025 calendar year, the $US firmed slightly last month. The absence of any indication of an immediate reduction in U.S. cash interest rates may have added support to the $US. This strength in the $US resulted in the $A declining from U.S. 65.5 cents to U.S. 64.7 cents. However, with the iron ore price increasing and some ongoing improvement in sentiment around the Chinese economic outlook, the $A was relatively well supported over the month and increased 2.1% against the Yen and was 1.3% higher relative to the Euro.

Outlook and Portfolio Positioning

The month of July was notable for the apparent lack of concern equity markets showed towards the looming finalisation of tariff agreements between the U.S. and the majority of its key trading partners. Although most tariffs have been set at levels below those announced in early April, the overall program remains highly significant. Tariffs as high as 50% on copper, aluminium and steel will have real impact, as will individual country tariffs such as the 35% charge on U.S. imports from Canada. In summary, the cost of living and inflation in the U.S. will be higher as a result, and economic growth lower.

Perhaps some of the rationale for the current resilience of the share market is derived from the view that the increasingly dominant U.S. technology sector is somewhat detached from the real economy and will prosper irrespective of any domestic inflation or cyclical downturn. Whilst there is logic to this view, the sector is not totally immune from shorter term economic cycles. For example, Meta and Alphabet (Google) are exposed to cyclically sensitive advertising spending; whilst Tesla, Apple and Amazon have direct exposure to U.S. consumer spending cycles. Notably, the “Magnificent 7” did all decline in value on the 1st of August when the release of worse than expected U.S. labour market data suggested some weakening in the U.S. economy may be occurring.

Whereas support for the U.S. technology sector continued unabated for most of July, there did appear to be a marked rotation in support at the larger company end of the Australian share market. After reaching a somewhat eye watering valuation, well beyond that which was comparable to domestic and international peers, support for the Commonwealth Bank did fall away in July, with the stock price falling 3.7% in an otherwise rising share market. Concurrently, there was a marked increase in support for both CSL and BHP, which are the two next largest stocks listed on the Australian exchange.

Although the finalisation of various tariff “deals” has removed one source of policy uncertainty, the lack of market response to the significant tariffs that are now locked in reinforces the need for a somewhat cautious approach to global equity markets. There remains a probability that weaker economic data in the U.S. may be at least a shorter-term outcome of the tariff regime, which could trigger a negative reaction on share markets (as per the response to the recent U.S. labour market data). The apparent rotation that may be taking place within the Australian equity market also has implications for portfolio positioning, as the environment may become more supportive of active management, with passive index-based strategies not able to respond to a change in market leadership.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), CSI China Securities 300 TR in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.