December 2025: Share markets post flat finish to the year

- There was little movement on global equity markets over December.

- Technology stocks once again lacked support and declined in value.

- Bond yields increased, with the margin on Australian bonds over US bonds widening further.

International Equities

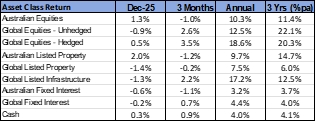

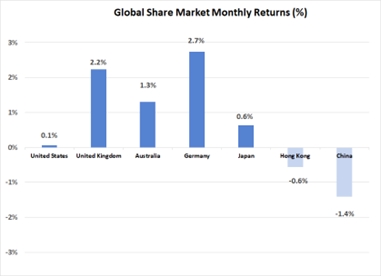

A cautious mood prevailed over equity markets during December, with the global developed market average advancing just 0.5% to bring the gain for 2025 to 18.6%. Europe made a strong contribution to this growth, with positive sentiment around the outlook for European economic growth boosting markets such as Germany (up 2.7%), Spain (up 5.8%) and Switzerland (up 3.2%).

Growth in the United States (up 0.1%) and Japan (up 0.6%) was less significant, with a 2.6% decline in the technology sector in the U.S. detracting from overall returns. Investors continue to show some concern over the magnitude of capital expenditure being made across the technology sector in Artificial Intelligence related infrastructure. There was also a reversal in support for some of the defensive sectors that rallied very strongly in November. For example, healthcare stocks fell by 2.3% and the consumer staples sector was 3.6% lower. In contrast, financial stocks rose 1.8%, which potentially reflected an easing in monetary conditions resulting from the U.S. Federal Reserve Bank’s decision to commence adding funds to money markets via a program of regularly purchasing Treasury Bills (also referred to as “Quantitative Easing”).

Although conditions on China’s share market continued to weaken, the overall MSCI Emerging Market Index outperformed the develop market average by advancing 1.3%. Healthy gains in South Korea (up 10.4%) and Taiwan (up 5.9%) offset the Chinese decline, with stocks such Samsung and TSMC (the Taiwanese semi-conductor manufacturer) posting impressive gains. India, though, capped off a year of underperformance with a flat result over December.

Higher bond yields in the United States led to declining prices for interest rate sensitive stocks. As a result, the global listed property asset class declined in value by 1.4%, with infrastructure falling 1.3%. Despite higher bond yields in Australia as well, the local listed property sector moved against the global trend in rising 2.0%. A 4.9% increase in Goodman Group, which makes up 34% of the Australian listed real estate index, was a major contributor to this growth. Goodman, which has a high exposure to data centre property, was a negative performer over much of 2025 following significant price growth in the previous two years.

Australian Equities

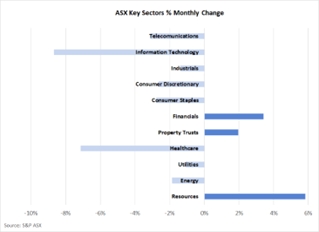

Following a period of underperformance, the Australian share market rose by more than the global average over December, with the S&P ASX 200 Index advancing 1.3%. On an annual basis, though, the Australian market still lags the global equity average return by 8.3%. As has been the case over recent months, resource stocks were the strongest contributor to the overall market. A slight 2.2% firming of the iron price, and a 5.3% jump in the gold price, contributed to the 5.8% gain in resource sector share prices.

Another period of weakness in the share price of CSL Limited (down 7.3%) had a negative impact on the healthcare sector overall. Although there was minimal stock specific news around CSL, its price appeared to be influenced by the global decline in the healthcare sector last month. Similarly, the fall globally in information technology stocks was also experienced domestically, with the Australian technology sector sold down by a significant 8.7%. In contrast, financial stocks were well supported, with the CBA (up 5.3%) partially reversing some recent weakness.

Fixed Interest & Currencies

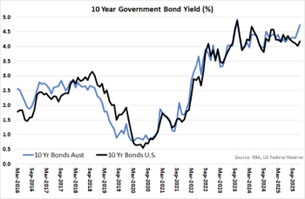

As per market expectations, the Australian Reserve Bank left cash interest rates unchanged at 3.6% at their board meeting in December. However, with inflation being higher than previously expected, market consensus is now firmly supporting an interest rate rise in the first half of 2026. As a result, longer term yields have continued to shift higher, with the Australian 10-year Government bond yield rising from 4.51% to 4.74% over December.

In contrast, the U.S. central bank did cut cash interest rates in December, with the target cash rate falling 0.25% to be within a range of 3.5% to 3.75%. Although U.S. 10-year Treasury Bond yields shifted slightly higher over the month, from 4.02% to 4.18%, yields are still below the levels prevailing earlier this year, with falls recorded in each of the previous 4 months. The 0.56% margin available on Australian 10-year yields over U.S. yields is the widest month-end gap recorded since June 2022.

Possibly due to the higher longer term Australian interest rates on offer, the $A appreciated in value over December. Against the $US, the $A rose U.S. 1.6 cents to U.S. 66.9 cents. The $A was also firmer against the Japanese Yen (up 1.2%) and the Euro (up 2.7%).

Outlook and Portfolio Positioning

December’s small gain on global equity markets completed the 3rd successive calendar year of strong market growth, which has seen returns from the global equity asset class average 20.3% per annum over these 3 years. Clearly, this rally is in a mature phase, with valuations extended. In addition, the pattern of recent market growth suggests investors are becoming much more circumspect around technology stocks and the potential for artificial intelligence related capital expenditure to drive earnings growth continuously higher.

However, despite some recent caution on equity markets, there remains a strong willingness by investors to continue push valuations higher, with the more recent focus being on those parts of the market that have been “left behind” and are trading more cheaply than the market average. The continuation of modest but positive economic growth, a well-functioning and liquid financial sector and the absence of any significant increase in credit defaults, may be all factors that explain the ongoing positive sentiment across share markets. In addition, policy remains generally supportive of share markets, with December’s loosening of monetary policy in the U.S. potentially very important. In addition to lowering the cash rate, the commitment made by the U.S. Federal Reserve to commence purchasing treasury bills may indicate a willingness of the central bank to support liquidity and bank lending, despite remaining uncertainties over the trajectory of U.S. inflation. With changes in the membership of the Federal Reserve Bank Board expected in 2026, market consensus believes that this supportiveness of equity and bond markets will continue, if not improve, further in the year ahead.

Australia is now somewhat out of step with the United States. Inflation here has picked up, despite subdued economic growth. Expectations of policy tightening (higher interest rates and more constrained government spending), combined with muted economic growth, is not a combination considered conducive to a strong performance on share markets. The less promising outlook for Australia has already been reflected on share markets to some degree. Australia’s recent share market underperformance would have been even more significant if not for a strong lift in the price of resource stocks (which has been partly driven by a surging gold price). One potential source of upside for the Australian share market is the possibility that inflation will re-commence its downward trajectory, thereby allowing a more supportive interest rate regime. This scenario would be a positive for both Australian share and bond valuations.

Although the outlook for global equities may continue to be brighter than that for the local market, there are factors that could disrupt the current broad support for global equities. One example is U.S. inflation, and the possibility that it could start to surprise on the upside. Another is the possibility that the ambitious earnings expectations underwriting the U.S. technology sector fail to materialise.

However, whilst it is instructive for investors to consider the possible risks and opportunities impacting market direction in the year ahead, it is normally the unknown (or non-forecastable) factors that have the most impact on markets. For example, 3 years ago, very few investors would have predicted the impact the development of artificial intelligence would have on share markets. Given the future influence of unknown risks and opportunities, investment strategies that pursue genuine diversification, with professional management and the ability to adjust exposures in a timely fashion, are likely to be the most successful over the longer term.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), MSCI China (Composite) in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665