August 2025: Resource stocks back in favour as China rallies

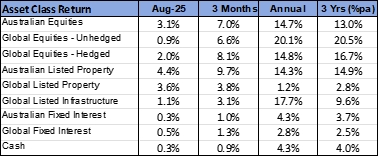

- Australian equities outperformed the global average, despite a volatile earnings reporting season.

- Positive momentum behind Chinese equities continued, which added support to resource stocks.

- Expectations of an interest rate reduction in the United States improved the outlook for U.S. cyclical stocks.

International Equities

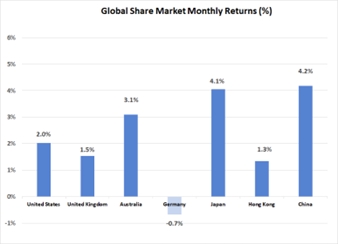

Although the steady gain in global equities continued over August, there was a shift in market leadership with the large technology sector underperforming. Nvidia, Meta, Microsoft and Amazon all posted negative returns over the month of between -2% and -5%. These losses were offset by gains in the U.S. healthcare sector, which rallied 6.1%, and financial stocks, which rose 4.2%. It was also a stronger month for smaller companies, with the U.S. Russell 2000 Index rising 7.1%. Firming expectations that the U.S. central bank will cut cash interest rates are likely to have added support to financials, cyclicals and smaller companies.

Outside of the U.S., share market performance was mixed. European markets were relatively flat, with both France and Germany slightly negative over August. However, results in parts of Asia were strong, with Japan’s Nikkei Index rising 4.1% and the Chinese market rallying 4.2%. There were also strong gains in South America, with higher commodity prices contributing. However, the overall Emerging Market Index was flat with continued negative returns in India (down 2.4%) offsetting gains elsewhere. The Indian market was negatively impacted by the news that the United States would be doubling the tariff applied to many imports from India to 50%. The tariff increase was made in response to India’s ongoing purchases of Russian crude oil.

Potentially buoyed by expectations of lower interest rates, real assets appreciated over August. Global listed real estate rose 3.6% over the month but remains the weakest of the major asset classes over a 1-year and 3-year time frame. The performance of Australian listed property was once again stronger, with the sector increasing 4.4%. Gains in global listed infrastructure were more modest at 1.1% .

Australian Equities

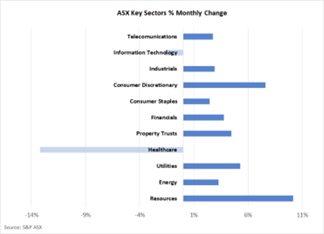

In an eventful earnings reporting season, the Australian market outperformed the global average over August, with the S&P ASX 200 Index rising 3.1%. In annual terms, Australian equities have increased by 14.7%, which is in line with the global average.

Contributing strongly to the local market outperformance were resource stocks, which rallied 10.2%. A 2.6% improvement in the iron ore price added support to the sector, as did improved confidence in the Chinese economy. Higher lithium and gold prices also helped buoy local mining companies.

The Consumer Discretionary sector (up 7.6%) was also well supported. Declining interest rates and signs of improved consumer confidence were positive for the sector, with Harvey Norman’s (up 18.8%) profit result being particularly well received. As was the case in the United States, it was also a strong month for smaller companies, with the Small Ordinaries Index rising 8.4%, with small gold mining companies making a major contribution to this.

Healthcare was the only sector finishing in negative territory last month. Following a 13.1% jump in July, CSL Limited was sold down by 21.4% in August, following a very negative reaction to the company’s annual results announcement. Although CSL’s earnings were only marginally below expectations, there were some indications of increased competitive pressure that may have led investors to lower growth forecasts for the years ahead. Additionally, an announced share buyback, cost reduction program and the sale of the Seqirus flu vaccination business, led investors to question growth expectations.

Within the financial sector, the rotation away from the Commonwealth Bank (down 2.8%) that commenced in late July continued through August. The other 3 major banks all appeared to be beneficiaries of this rotation, with price gains recorded of between 9.6% and 14.2%.

Fixed Interest & Currencies

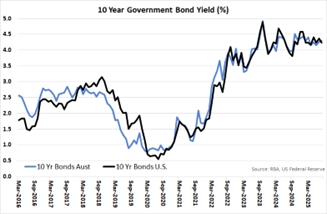

Conditions on bond and money markets were stable over August. As expected, the Reserve Bank of Australia reduced the target cash interest rate from 3.85% to 3.60%. Longer term interest rates were steady, with the Australian 10-year government bond yield closing the month at 4.30%. However, in the U.S., commentary from the Federal Reserve Chairman indicated a more “dovish” view on monetary policy and expectations of a cash rate reduction this year increased. As a result, longer term yields adjusted lower, with the U.S. 10-year treasury bond yield falling from 4.37% to 4.23%.

Conditions on bond and money markets were stable over August. As expected, the Reserve Bank of Australia reduced the target cash interest rate from 3.85% to 3.60%. Longer term interest rates were steady, with the Australian 10-year government bond yield closing the month at 4.30%. However, in the U.S., commentary from the Federal Reserve Chairman indicated a more “dovish” view on monetary policy and expectations of a cash rate reduction this year increased. As a result, longer term yields adjusted lower, with the U.S. 10-year treasury bond yield falling from 4.37% to 4.23%.

Possibly due to the slightly lower U.S. bond yields, there was a renewed softening in the value of the $US over August. This enabled the $A to appreciate from U.S. 64.7 cents to U.S. 65.4 cents. However, the $A was slightly weaker against the Yen and the Euro by 0.1% and 1.0% respectively.

Outlook and Portfolio Positioning

Financial market conditions have continued to be rewarding for investors, with August being another month in which all major asset classes delivered positive returns. There was some shift in sentiment, however, with a loss of momentum in the U.S. technology sector being offset by a more positive view on the likelihood of a U.S. interest rate cut. The firming of expectations of lower U.S. interest rates does, however, further increase the policy risk imbedded into current equity market valuations. Notwithstanding Jerome Powell’s (U.S. Federal Reserve Chairman) comments at the Jackson Hole Economic Symposium suggesting that the “balance of risks to the American economy was shifting”, an interest rate reduction should not be considered a certainty. With U.S. economic and employment growth still robust, and the impact of tariffs on inflation still unknown, it could be argued that the prudent path for the central bank would be to leave cash interest rates unchanged for now.

In addition to the possibility that a U.S. interest rate reduction may take longer than financial markets are now anticipating, other U.S. policy risks should be carefully considered by investors. The impact of the tariff program on inflation and economic growth remains uncertain, with the recent ruling by the U.S. Court of Appeals that much of the tariff program is not legal adding further complexity to this assessment. The possibility of an enforced wind-back of parts of the tariff program may also increase the focus on the U.S. Government’s fiscal position, which would come under pressure as a result of any material loss of expected tariff revenue. This, in turn, could challenge the current optimism of U.S. bond markets.

Domestically, the share market’s recent focus has been on company result announcements. The reporting season was notable for the exceptionally large price response to earnings surprises. A common theme in the price response was that the market is less willing to pay high multiples on the “promise” of earnings growth that was not backed by tangible evidence of solid progress towards those growth expectations . This pattern of response could be indicative of a collective market concern that valuations had moved ahead of fundamentals in an economic environment that was not conducive to earnings growth being easily achieved.

Although overall share market valuations could still be viewed as being based on overly optimistic assumptions that fail to fully account for significant U.S. policy related risks, the recent price movements within equity markets does demonstrate a degree of market rationality. Areas of undervaluation, such as Australian resources, smaller companies, and Chinese equities, have appreciated. Conversely, the market has not simply kept rewarding those stocks and sectors that have performed so well over recent quarters – such as U.S. technology and the Commonwealth Bank. In this environment, portfolio strategies that are more focussed on assessing fundamental opportunities and risks, rather than simply following market momentum, may be well rewarded.

Important Information

The following indexes are used to report asset class performance: ASX S&P 200 Index, MSCI World Index ex Australia net AUD TR, MSCI World ex Australia NR Hdg AUD, FTSE EPRA/NAREIT Developed REITs Index Net TRI AUD Hedged, Bloomberg AusBond Composite 0 Yr Index, Barclays Global Aggregate ($A Hedged), Bloomberg AusBond Bank Bill Index, S&P ASX 300 A-REIT (Sector) TR Index AUD, S&P Global Infrastructure NR Index (AUD Hedged), MSCI China (Composite) in CN, Deutsche Borse DAX 30 Performance TR in EU. Hang Seng TR in HKD, MSCI United Kingdom TR in GBP, Nikkei 225 in JPY, S&P 500 TR in USD.

General Advice Disclaimer

Any advice contained in this document is of a general nature only and does not take in to account the objectives, financial situation or needs of any particular person. Any decision to invest in products mentioned in this document should only be made after reviewing the relevant Product Disclosure Statements. Past performance is not a reliable indicator of future performance. Varria Pty Ltd is an authorised representative of Charter Financial Planning ABN 35 002 976 294 AFSL number 234665